July 2023

This article discusses the two cash management approaches our Global Family Office group is seeing in use among top family offices.

With the most aggressive tightening cycle in over 40 years creating attractive short-term yields unseen for decades, one of the most frequent questions we hear from single family offices at BNY Mellon Wealth Management is: “How are my peers thinking about liquidity management?”

While every family office investment program is different, our Global Family Office group sees common approaches to supporting cash needs efficiently in a timely manner while maximizing yield. The first approach is to accept what the market provides and spend as little time as possible thinking about managing liquidity. The second approach involves organizing cash into different buckets based on expected use of that cash to maximize after-tax yield.

Framework #1: Keep It Simple

Prior to the start of the 2022 interest rate hiking campaign, when short-term interest rates were ~0%, the only way to capture a meaningful yield on cash was to increase credit and/or duration risk. While some offices were comfortable with this, others opted to keep it simple and invest in some combination of money market funds and short-term Treasuries, and/or maintain cash reserves in bank deposit programs.

The rationale we hear from family offices that have decided to keep it simple is that they believe the opportunity cost to not keeping it simple is too high: time spent on managing their liquidity program is time they do not spend on investments with higher alpha-potential where they may have a competitive edge (e.g., their operating business or direct investing). Given this trade-off, they prefer to keep it simple and spend their time elsewhere.

Framework #2: Liquidity Bucketing

On the other hand, there are many family offices that believe it is worth the time to create a custom bucketing framework to maximize liquidity and after-tax yield on their cash while considering planned (and unplanned) spending needs. Additionally, liquidity bucketing provides the family office with flexibility so that they are not forced to redeem investments at inopportune times, such as during market dislocations. The framework is also transparent: with the reasoning for each bucket – and the holdings within it – clearly delineated.

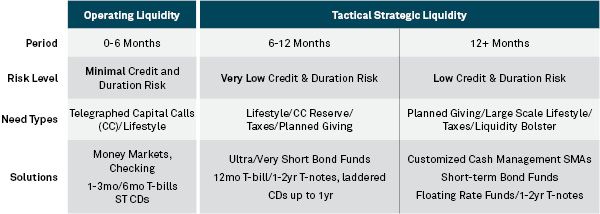

For clients who subscribe to the liquidity bucketing approach, the general framework is: 1) match the duration of the asset (e.g., cash) with the duration of the liability (e.g., expected cash usage) and 2) select investments within each bucket that incrementally, and prudently, increase the credit and/or duration risk to maximize the after-tax yield. While true cash should be used to fund day-to-day liabilities, as cash buckets extend into the future the family office can choose to allocate to ultrashort and short-term bond holdings or other solutions (see Exhibit 1).

Exhibit 1: Example of Cash & Near Cash Bucketing

Source: BNY Mellon Wealth Management, 2023.

Customization and Control

Amid the shifting interest rate environment, we have observed an increased adoption of the liquidity bucketing approach. The reason is twofold:

1. More customization based on discrete cash flow and liquidity needs

2. More control and transparency via separately managed accounts (SMAs)

We have also seen higher demand for customized SMAs. These separately managed accounts provide the investor with increased control and transparency over their investments (e.g., they are able to sell specific securities to meet liquidity goals versus having to partially redeem a mutual fund). This increased control might lead to tax advantages, depending on the gain/loss disposition of the securities available within the SMA. Additionally, a separately managed account can inoculate an investor against “flow risk,” whereby investor redemptions from a fund could adversely affect other investors since a portfolio manager might need to sell securities at inopportune times to meet liquidation requests.

A potential downside of incorporating a custom SMA into a liquidity management program is that it may introduce additional operational and reporting complexity. For example, an investor might receive a bulky statement with many line items, making consolidated reporting and risk monitoring cumbersome. Our Global Family Office group can help clients fully mitigate these operational issues and simplify the process.

Considering Your Liquidity Management Options

Liquidity management has never been more important than it is today. As a leader in cash management strategies, separately managed accounts and tailored lending solutions, we welcome the opportunity to discuss ways to potentially enhance your liquidity management program.

Click here to download a PDF of this article

This material is provided for illustrative/educational purposes only. This material is not intended to constitute legal, tax, investment, or financial advice. Effort has been made to ensure that the material presented herein is accurate at the time of publication. However, this material is not intended to be a full and exhaustive explanation of the law in any area or of all the tax, investment, or financial options available. The information discussed herein may not be applicable to or appropriate for every investor and should be used only after consultation with professionals who have reviewed your specific situation.

The Bank of New York Mellon, DIFC Branch (the “Authorized Firm”) is communicating these materials on behalf of The Bank of New York Mellon. The Bank of New York Mellon is a wholly owned subsidiary of The Bank of New York Mellon Corporation. This material is intended for Professional Clients only and no other person should act upon it. The Authorised Firm is regulated by the Dubai Financial Services Authority and is located at Dubai International Financial Centre, The Exchange Building 5 North, Level 6, Room 601, P.O. Box 506723, Dubai, UAE.

The Bank of New York Mellon is supervised and regulated by the New York State Department of Financial Services and the Federal Reserve and authorized by the Prudential Regulation Authority. The Bank of New York Mellon London Branch is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request. The Bank of New York Mellon is incorporated with limited liability in the State of New York, USA. Head Office: 240 Greenwich Street, New York, NY, 10286, USA.

In the U.K. a number of the services associated with BNY Mellon Wealth Management’s Family Office Services– International are provided through The Bank of New York Mellon, London Branch, One Canada Square, London, E14 5AL. The London Branch is registered in England and Wales with FC No. 005522 and BR000818.

Investment management services are offered through BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, One Canada Square, London E14 5AL, which is registered in England No. 1118580 and is authorised and regulated by the Financial Conduct Authority. Offshore trust and administration services are through BNY Mellon Trust Company (Cayman) Ltd.

This document is issued in the U.K. by The Bank of New York Mellon. In the United States the information provided within this document is for use by professional investors.

This material is a financial promotion in the UK and EMEA. This material, and the statements contained herein, are not an offer or solicitation to buy or sell any products (including financial products) or services or to participate in any particular strategy mentioned and should not be construed as such.

BNY Mellon Fund Services (Ireland) Limited is regulated by the Central Bank of Ireland BNY Mellon Investment Servicing (International) Limited is regulated by the Central Bank of Ireland.

Trademarks and logos belong to their respective owners.

BNY Mellon Wealth Management conducts business through various operating subsidiaries of The Bank of New York Mellon Corporation.

©2023 The Bank of New York Mellon Corporation. All rights reserved. | WM-400731